🏈 A Rough Start Out of the Gate

If there’s one team that captures the spirit of the markets in 2025, it’s the Chicago “Monsters of the Midway” Bears. The year began with a false start. Early missteps, policy uncertainty, and stubborn inflation pressures caused markets to fumble out of the gate. Confidence waned, volatility spiked, and by the end of the first quarter, many investors felt like portfolios had gone three-and-out.

Tariff concerns, shifting interest-rate expectations, and elevated valuations kept markets pinned deep in their own territory. Risk appetite faded, defensive positioning became more attractive, and the broader narrative turned cautious. Much like the Bears’ early-season struggles, the opening stretch of 2025 left investors wondering whether this would be another rebuilding year.

🏈 Finding an Identity at Midfield

As the year progressed, both the Bears and the markets began to regroup and adjust their game plan. For Chicago, that meant tightening execution and leaning into strengths. For markets, it meant recalibrating expectations as earnings proved more resilient and economic growth continued to move the chains.

Even as momentum shifted, markets continued to test investors’ nerves — much like the “Cardiac Bears,” capable of thrilling comebacks but rarely without stress. Artificial intelligence emerged as a true difference-maker, the market’s franchise quarterback. As productivity gains and long-term innovation potential became clearer, AI-driven companies helped stabilize sentiment and restore confidence.

What started as a cautious, short-yardage approach evolved into sustained drives that pushed markets back toward midfield and beyond. By midyear, momentum had clearly shifted. Investors weren’t calling trick plays — but they were willing to take more risk as the fundamentals improved and the offense found its rhythm.

🏈 The Second-Half Surge: How the Asset Classes Performed in 2025

Like any good comeback story, the second half of 2025 belonged to execution. Early in the year, defense mattered most. As confidence returned, offense took over and carried the game into year-end. Different asset classes contributed at different moments, but together they put points on the board. As the clock expired on the 2025 season, here’s how the Scoreboard looked:

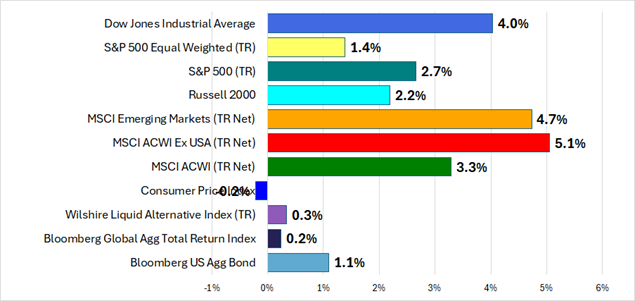

4Q25 Benchmark Returns

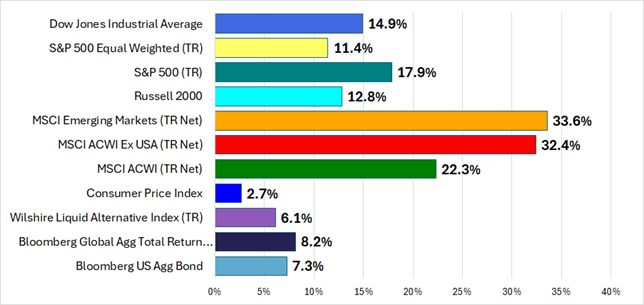

2025 Benchmark Returns

U.S. equities finished 2025 as the clear offensive leaders. After a challenging first few months marked by tariff concerns, inflation uncertainty, and valuation pressure, stocks mounted a sustained drive beginning in mid-April and never really looked back. All major benchmarks were over double-digits, e.g. the Russell 2000 Small Cap registered a 2.2% 4Q25 & 12.8% 2025 return, while the large-cap market-cap weighted SP500 rose 2.7% 4Q25 & 17.9% 2025! Large-cap growth and technology stocks led the charge, with AI calling the plays at the line of scrimmage. Earnings growth and margin resilience helped markets consistently convert on third down, pushing major indexes to strong full-year gains. That said, leadership remained concentrated, leaving little room for error if expectations slip or sentiment turns.

International equities steadily – and significantly – moved the chains. With more attractive valuations and improving momentum in select regions, overseas markets delivered solid results over the full year as represented by the 5.1% 4Q25 & 32.4% 2025 increases in the MSCI AC World Ex-USA Index! Shifts in global trade dynamics following tariff developments created opportunities abroad, even as currency movements and divergent central-bank policies added complexity.

Fixed income was the Bears’ defense in 2025 — disciplined, relentless, and far more impactful than anyone expected coming into the season. While markets focused on the flashier offensive storylines, bonds quietly delivered strong, consistent returns throughout the year – evidenced by the strong Barclays US Aggregate Bond Index up 1.1% 4Q25 & 7.3% 2025 – as inflation pressures eased and the Federal Reserve signaled greater flexibility. Like a defense that forces turnovers and occasionally scores itself, fixed income provided both stability and upside — an outcome that exceeded most expectations and reinforced its role as an active return contributor, not just a risk mitigator.

Alternative investments were far more than complementary pieces in 2025 — and gold*, in particular, was a game-changer. If fixed income was the Bears’ dominant defense, gold was the turnover returned for a touchdown! With prices rising roughly 60% on the year, gold delivered one of the strongest performances across all asset classes, benefiting from persistent inflation concerns, geopolitical uncertainty, central-bank demand, and waning confidence in fiat currencies. Rather than merely hedging risk, gold consistently put points on the board, validating its role as a core allocation within our DWM Liquid Alternatives portfolio. Other alternatives – like event-driven hedged funds** (+1.6% & 8.4%) and market-neutral funds*** (+1.6% & 6.4%) – moved the chains forward in a steady, meaningful way.

Putting it all together, diversified investors had a season worth celebrating. Gains came from multiple units — equities drove the offense, fixed income anchored the defense, and gold delivered momentum-changing plays. The result for many portfolios was a convincing victory, finishing the year up one to two touchdowns!

🏈 Playoff Football: No Margin for Error Heading Into 2026

As 2025 comes to a close, both the markets and the Chicago Bears find themselves in playoff mode. What began as a season defined by early mistakes evolved into a hard-earned comeback, carrying momentum into a do-or-die moment. For the Bears, that means facing their longtime rival, the Green Bay Packers. For investors, it means entering 2026 with markets in the red zone — but with expectations, valuations, and emotions all running high.

The gains in 2025 were well deserved. Earnings proved resilient, economic growth held up, fixed income delivered unexpectedly strong results, and innovation — particularly in artificial intelligence — reshaped long-term assumptions. But playoff football leaves no margin for error. Elevated valuations, concentrated leadership, and an ever-changing macro backdrop mean that execution matters more than ever. A missed assignment or forced throw can quickly change field position. At the same time, renewed U.S.–Venezuela tensions serve as a reminder that geopolitical risk remains a live factor for markets, capable of introducing volatility and shifting investor sentiment with little warning.

This is not the time for a Hail Mary — but it’s also not the time to punt on discipline. Successful teams rely on preparation, balance, and discipline when the pressure is highest. At DWM, that means staying true to the fundamentals that guided portfolios through both the early-season struggles and the late-season surge: diversification across asset classes, thoughtful rebalancing, and a long-term focus that avoids chasing short-term momentum.

Markets, like playoff games, are inherently unpredictable. But over full seasons — and full market cycles — disciplined strategies tend to win more often than not. As we head into 2026, the objective isn’t to predict every play, but to remain well positioned, adaptable, and ready to respond as conditions evolve. The comeback in 2025 was impressive — now it’s about executing cleanly when it matters most. And just as the Bears’ turnaround has been fueled by elite coaching and execution, investors working with DWM are better positioned to execute successfully when the stakes are highest.

Let’s go Bears!

Brett M. Detterbeck, CFA, CFP®

DETTERBECK WEALTH MANAGEMENT

* represented by the iShares Gold Trust

** represented by the BlackRock Event Driven Fund

*** represented by the Victory Market Neutral Income Fund