First Pitch: A Season of Surges and Slumps

Much like the Chicago Cubs’ 2025 season, the stock market’s path this year has been anything but linear. January opened with confidence — economic data came in strong, the Fed appeared poised to pivot, and investors took their swings with conviction. But by March, that optimism faded. Growth cooled, and the rally that had started the year so brightly suddenly found itself in a slump. It felt like a cold streak at Wrigley in early spring — the fundamentals hadn’t disappeared, but the timing wasn’t clicking.

Then came April — and with it, Trump’s Liberation Day. Markets opened that week to sweeping tariff headlines and a wave of uncertainty. Stocks stumbled sharply as investors recalibrated the risks to global trade and corporate margins. The initial reaction was swift and punishing, reminiscent of a team giving up a bases-clearing triple just when momentum seemed to be building. But just as quickly, resilience returned. Within weeks, markets shook off the blow, reassured by strong earnings and a still-resilient consumer.

From that point forward, the rally took on new life — powered largely by artificial intelligence and the companies driving its adoption. Like a phenom slugger anchoring the lineup, AI became the market’s MVP, delivering both earnings strength and narrative fuel. Productivity optimism, technological disruption, and a sense that innovation could outrun macro headwinds helped turn a shaky spring into a red-hot summer.

Now, as autumn arrives, both the Cubs and the markets find themselves in similar territory: riding high, but on edge. Valuations have stretched to historically elevated levels, leaving little room for error if the next pitch — or data print — breaks the wrong way. The AI leaders have carried the offense, while many other sectors are still waiting for their turn at bat. As the season heads into its late innings, investors face the same question the Cubs do: can this remarkable run keep going, or are we one game away from disappointment? But before we ponder that question, let’s check the 2025 Scoreboard:

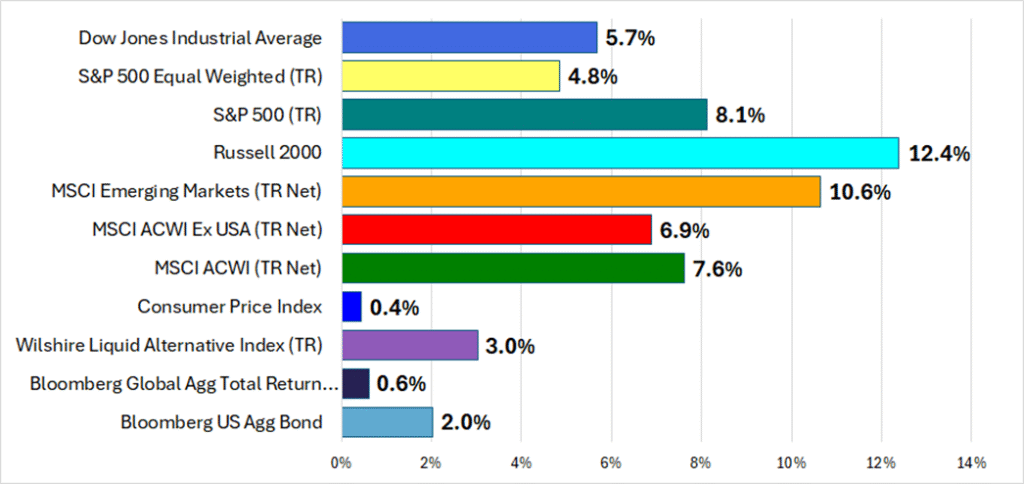

3Q25 Benchmark Returns

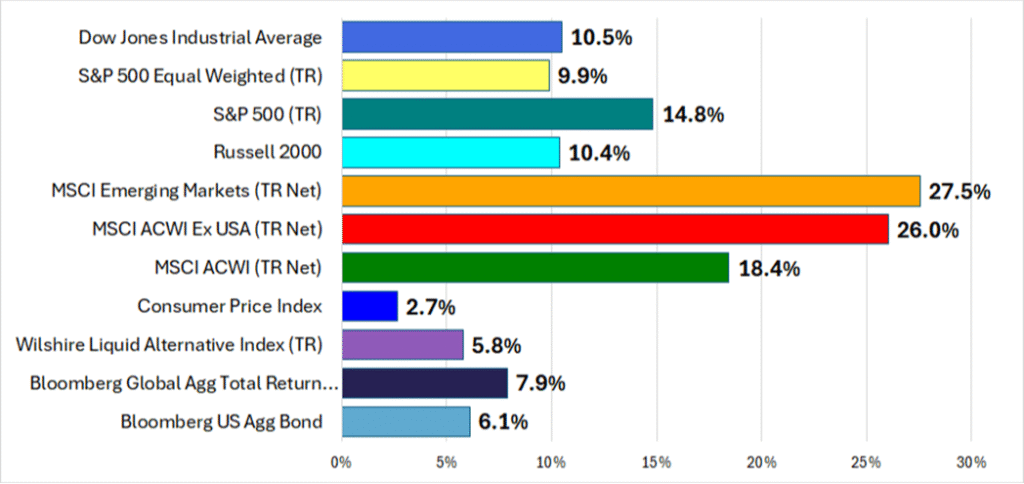

YTD Benchmark Returns

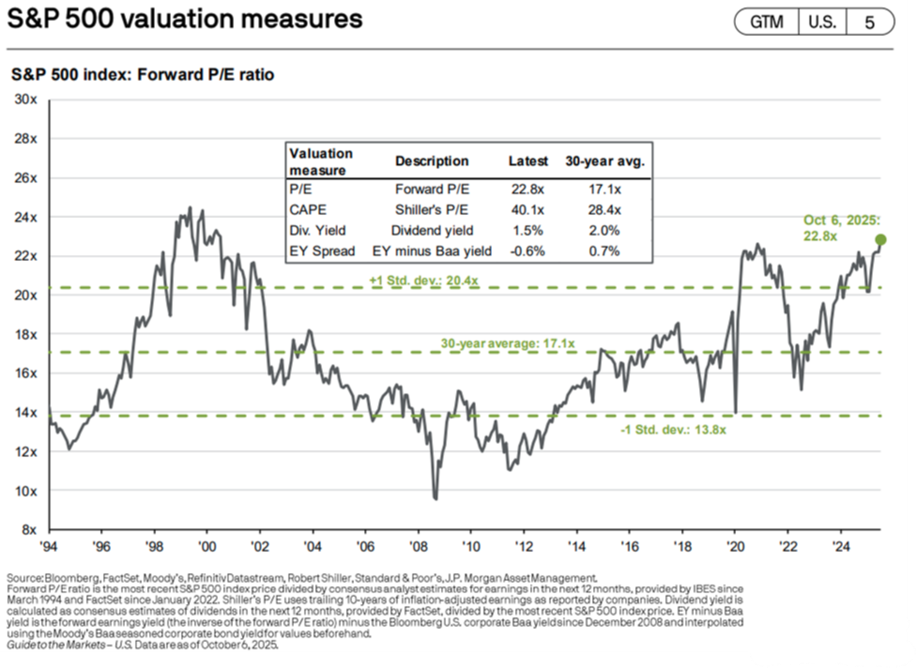

U.S. equities have delivered strong returns overall, shaking off their March-April slump with an impressive mid-season surge. The S&P500 blasted out an 8.1% 3Q25 return & is now up 14.8% YTD! The rebound was led by large-cap growth and technology stocks, particularly those connected to artificial intelligence. These “cleanup hitters” have been hitting homeruns, turning in blockbuster earnings and fueling optimism that AI-driven productivity could sustain growth even as policy and inflation remain uncertain. Yet, much like a lineup that leans too heavily on its stars, the market’s breadth remains narrow. Valuations for these AI leaders have stretched to levels reminiscent of prior late-cycle peaks, leaving investors vulnerable if expectations slip. From the chart below, you can see that the forward P/E on the S&P500 has only been higher than now once over the last few decades.

Small-cap, value, and cyclical stocks have lagged by comparison, but perhaps are just now taking advantage of their turn at bat. For example, the Russell 2000 US Small Cap Index is “only” up 10.4% YTD but that’s after a towering 12.4% third quarter return. Higher borrowing costs, uneven economic data, and the gravitational pull of mega-cap dominance have kept these groups on the defensive. But history reminds us that market leadership tends to broaden as the cycle matures. Should rate-cut expectations solidify or earnings leadership rotate, these underappreciated players could be poised for more late-season heroics.

International equities have quietly delivered amazing results (as evidenced by the MSCI AC World Index, up 6.9% in 3Q25 & 26.0% YTD), supported by more attractive valuations and, in some regions, improving economic momentum. The renewed focus on trade following Trump’s “Liberation Day” tariff announcements has also reshaped expectations, with certain export-oriented economies benefiting as global supply chains adjust. Currency dynamics and divergent central-bank policies continue to add complexity, but for long-term investors, the relative value argument abroad remains compelling.

Fixed income has provided a stabilizing presence in the portfolio — the bullpen, so to speak. And like the Cubs bullpen for the last couple of months; most of the fixed income subcategories like government, corporate, securitized debt, etc. have performed relatively strong! For the record, the US Aggregate Bond Index recorded a 2.0% 3Q25 return & is now up 6.1% for the year.

Alternatives, at least the basket of liquid alternatives we follow – in PCA fashion – continue their break-out year! Our significant holding in gold (up 16.7% in 3Q25 & now up over 47% YTD!) has shined the brightest! The fall of the US Dollar and the rise of populism are reasons for gold’s ascent. We have also seen good performances out of real estate* (up 8.1% YTD) and some hedged alternative strategies (like long/short** up 11.3% YTD.) In an equity market that has been heavily momentum-driven, these uncorrelated exposures remain valuable players off the bench.

Seventh-Inning Stretch: Staying Disciplined in a Late-Cycle Market

As we head into the final innings of 2025, both the Cubs and the markets remind us that momentum can be fragile. A few bad pitches (“Aye yi yi, Imanaga”) – whether in the form of inflation surprises, geopolitical curveballs, or policy missteps — could easily shift sentiment. Yet just as a playoff-bound team stays focused on fundamentals, investors should resist the urge to overreact to short-term noise. Winning seasons are built not on one hot streak, but on consistent execution, adaptability, and patience through volatility.

The economic scoreboard still shows more positives than negatives. The backdrop for stocks remain solid, with prospects for more Fed rate cuts (perhaps two more in 2025 and a couple in 2026), growing corporate profits, and fading tariff uncertainty. The AI revolution continues to reshape business models and drive productivity gains that could prove more enduring than skeptics expect. However, with valuations elevated and concentration risk high (the top 10 names within the S&P500 represent over 40% of its market cap!), this is not the time to swing for the fences. Staying diversified, rebalancing thoughtfully, and emphasizing quality — in equities, fixed income, and alternatives — are key to navigating the innings ahead. Just like a quality manager like the Cubs’ Craig Counsel can better your baseball team, make sure you have a strong coach like DWM to tend to your portfolio!

For Cub fans, this particular moment feels a little bit like our backs against the wall. For long-term investors, this moment feels less like the bottom of the ninth and more like a tight game entering extra innings. There will be rallies and retracements, leadership shifts and surprises, but the teams that endure — and the portfolios that outperform — are those that remain balanced, disciplined, and ready to play all nine innings.

Manager’s Note

At DWM, we’re staying true to our playbook. The past year has offered its share of curveballs — from tariff surprises to shifting inflation data — but it’s also reminded us that strong teams (and strong portfolios) win through patience, balance, and fundamentals. We continue to favor diversified exposure across asset classes, disciplined rebalancing, and selective participation in the most compelling long-term themes — including the transformative potential of artificial intelligence.

Just as the Cubs know that every inning counts, we recognize that markets reward those who stay in the game, even when conditions get unpredictable. Our focus remains on helping clients reach their goals — not by chasing every rally, but by positioning portfolios to endure and prosper over the full season.

Thank you, as always, for your continued trust and partnership. From all of us at DWM, we wish you and the Cubs a strong finish to 2025.

Brett M. Detterbeck, CFA, CFP®